Five-year arbitrage rebate reporting stands as a key milestone that demands careful attention within your bond compliance process. Within the last five years, we have witnessed both low borrowing rates and a sharp increase in the federal funds rate. This drastic change in the rate environment could mean that your unspent proceeds are quietly racking up a costly arbitrage rebate bill.

Understanding the five-year reporting requirements and their implications can be the difference between seamless compliance and costly penalties. We’ve compiled a complete guide for municipal bond issuers to aid in maintaining compliance and prepare you for any potential payments well in advance of your 5th-year reporting period.

Understanding Arbitrage Rebate Reporting Fundamentals

Arbitrage occurs when issuers invest tax-exempt bond proceeds in higher-yielding investments, potentially generating excess earnings. The IRS requires that these excess earnings be calculated and, if applicable, rebated to the federal government or offset through yield restriction measures. This requirement ensures that issuers don’t unfairly profit from their tax-exempt status, while maintaining the integrity of the municipal bond market.

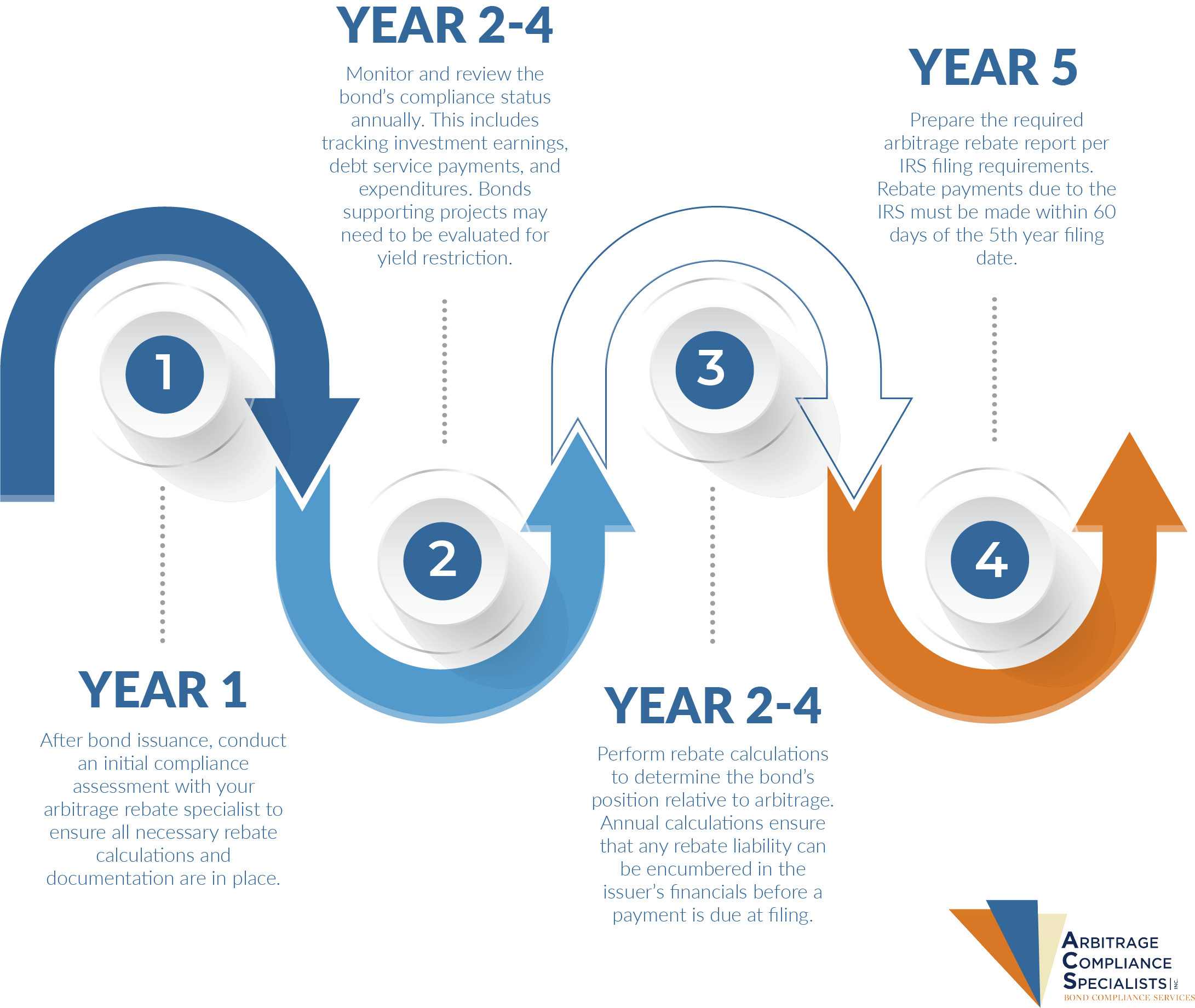

The five-year reporting requirement serves as a mandatory checkpoint for issuers to evaluate their arbitrage earnings and determine any rebate obligations. This timeline isn’t arbitrary, it provides a structured approach to compliance while allowing enough time for accurate calculations and proper documentation.

With the Federal Reserve increasing interest rates over the past few years to combat inflation, many issuers may now face higher-yield investment opportunities, increasing the potential for arbitrage liability to accrue. If your bonds were issued in early 2020 or 2021, now is the time to conduct a thorough arbitrage rebate calculation to assess your compliance status.

Critical Components of Five-Year Reporting

Several factors (namely time, balance, and investment yield) determine whether your bonds will require an arbitrage rebate payment or if yield restriction is necessary to limit investment earnings. By adopting a proactive approach to your bond compliance, you can help mitigate potential liabilities and ensure compliance with IRS regulations. By taking control of your portfolio, you’ll gain an accurate assessment of your position in terms of positive or negative arbitrage, allowing you to make calculated decisions before required IRS deadlines.

Below are critical components of the five-year reporting process that help to ensure you approach your reporting period with confidence.

Comprehensive Record Keeping

To ensure successful five-year arbitrage rebate reporting, issuers should adopt several best practices that can streamline the process and promote compliance. First and foremost, establishing a comprehensive record-keeping system is essential. This system should capture all relevant information related to bond proceeds, investments, expenditures, and revenues.

These records should be reviewed and updated yearly to include earnings, expenditures and debt service payments. If your bond is supporting a project, you may need to evaluate for yield restriction as well.

Maintaining detailed records of all bond-related transactions is essential. This includes:

- Initial bond issuance documentation (IRS Form 8038 or 8038-G, Tax Certificate, Official Statement, CPA Verification Report)

- Investment transactions and earnings, with a running balance

- Expenditures

- Debt service payments

- Previous annual calculations and reports

Annual Calculations

Performing annual rebate calculations will help you determine your bond’s position relative to arbitrage. If your investment is earning above your bond’s calculated yield, you are likely earning positive arbitrage on that investment. However, that single investment is blended together with all other investments funded with proceeds of the issue in determining your rebate liability. These annual calculations ensure that any rebate liability can be encumbered in the issuer’s financials before a payment is due at filing.

This not only reduces the risk of unexpected financial obligations but also provides a clear roadmap for managing bond proceeds effectively. Annual calculations streamline the final reporting process, ensuring that issuers are prepared to meet IRS deadlines with confidence.

The core of five-year reporting lies in precise annual calculations that determine:

- Bond yield, if not fixed at issuance

- Investment yield

- Net arbitrage earnings

- Applicable spending exceptions and adjustments

- Final rebate amount, if any

Timeline Management

Staying compliant with arbitrage rebate requirements means keeping a close eye on critical deadlines. One key milestone is the five-year reporting date, after which any rebate payments owed must be made within 60 days of the computation date. The first rebate installment payment must be made no later than the fifth anniversary date of a bond issuance. Subsequent five-year rebate and/or yield restriction payments must be made to the IRS no later than 60 days after the five-year anniversary from the previous computation date.

An issuer must repeat the five-year calculation reporting process for each subsequent five-year period and upon the final maturity of any tax-exempt financing. If it is determined that an arbitrage rebate payment is due, you are required to file form 8038-T with the IRS and submit the necessary payment.

Missing this deadline can result in penalties, such as late interest and 50% of the unpaid rebate amount on untimely filings. In extreme cases, the IRS can deem your bonds “taxable”, requiring an Issuer to pony up the difference in borrowing costs from the issuance date forward. That’s why it’s so important to know your upcoming deadlines and to plan ahead. Establishing a consistent schedule for annual calculations and reviews ensures you’re well-prepared to meet this and other reporting requirements. By adhering to a structured timeline, issuers can avoid last-minute surprises and remain compliant with IRS regulations.

Meeting the five-year deadline requires careful, long-term planning. Issuers should:

- Maintain detailed documentation including reporting deadlines

- Schedule annual calculations to identify potential issues early

- Allow sufficient time for professional review and report preparation

- Plan for timely submission to the IRS

Managing Arbitrage Compliance

Managing arbitrage compliance in-house can be challenging, especially with evolving IRS regulations and the complexities of investment earnings and rebate calculations. There are numerous unique situations for each bond issue that require careful review and precise calculation. That’s why many organizations turn to Arbitrage Compliance Specialists for expert support.

For nearly 40 years, ACS has been the trusted partner of municipalities across the U.S. in managing their arbitrage compliance and five-year reporting requirements. Our staff is experienced in complex bond issues and stands committed to helping our clients reduce their liabilities to the lowest amount allowable by law.

Partnering with ACS offers:

- Comprehensive Knowledge: Our team has a deep understanding of IRS regulations, ensuring accurate compliance with every calculation and report.

- Advanced Tools: We utilize cutting-edge calculation tools and methodologies to deliver precise and reliable results.

- Expertise with Complex Scenarios: Whether it’s managing multiple bond issues or navigating unique investment situations, we bring decades of experience to the table.

- Audit Support: In the event of an IRS audit, we provide the documentation and expertise you need for a seamless process.

- Peace of Mind: With ACS managing your annual and five-year reporting requirements, you can focus on other priorities, confident that your compliance needs are handled by professionals.

Trust ACS to help you stay ahead of deadlines and ensure your arbitrage compliance is managed with the highest level of accuracy and care.

Approach Compliance With Confidence

Five-year arbitrage rebate reporting represents a key milestone of municipal bond compliance. Success requires a combination of careful planning, accurate calculations, and proper documentation. By understanding the requirements, implementing proactive processes, and leveraging appropriate resources, issuers can maintain compliance while safeguarding the tax-exempt status of their bonds.

By partnering with ACS, you gain access to industry-leading expertise, meticulous attention to detail, and a proven process to ensure seamless compliance with your five-year reporting deadlines.

If your bonds were issued in early 2020 or 2021, now is the ideal time to begin preparing for your fifth-year computation. At Arbitrage Compliance Specialists, Inc., our team is dedicated to helping municipal organizations like yours maintain compliance across your entire bond portfolio. Reach out to schedule a consultation with our experienced arbitrage compliance specialists and start planning your next calculation today.